1.2 Revenue raising using tax measures generating sustainable financing for health promotion

Welcome. The speaker for this module is Ms Anne-Marie Perucic, Economist, World Health Organization (WHO).

Choose between video, audio or transcript to learn about this section.

Audio:

Hi again, my name is Anne-Marie Perucic, I am from the World Health Organization (WHO). Previously, we have learned about the global health expenditure and funding sources. We will now be looking at “Revenue raising using tax measures generating sustainable financing for health promotion”, that is, looking specifically at how health taxes can contribute to sustainable financing but of course, to a certain extent and with some limitations.

Let’s first start with why we need sustainable financing for health. Health is an investment and sustainable health financing is, therefore, economically compelling. Health financing is sustainable when increases in health expenditure can be maintained and are matched by corresponding increases in domestic revenues. Health financing may not be sustainable when increases in health spending are overly reliant on debt or overseas development assistance as we have seen before is the case for low-income countries.

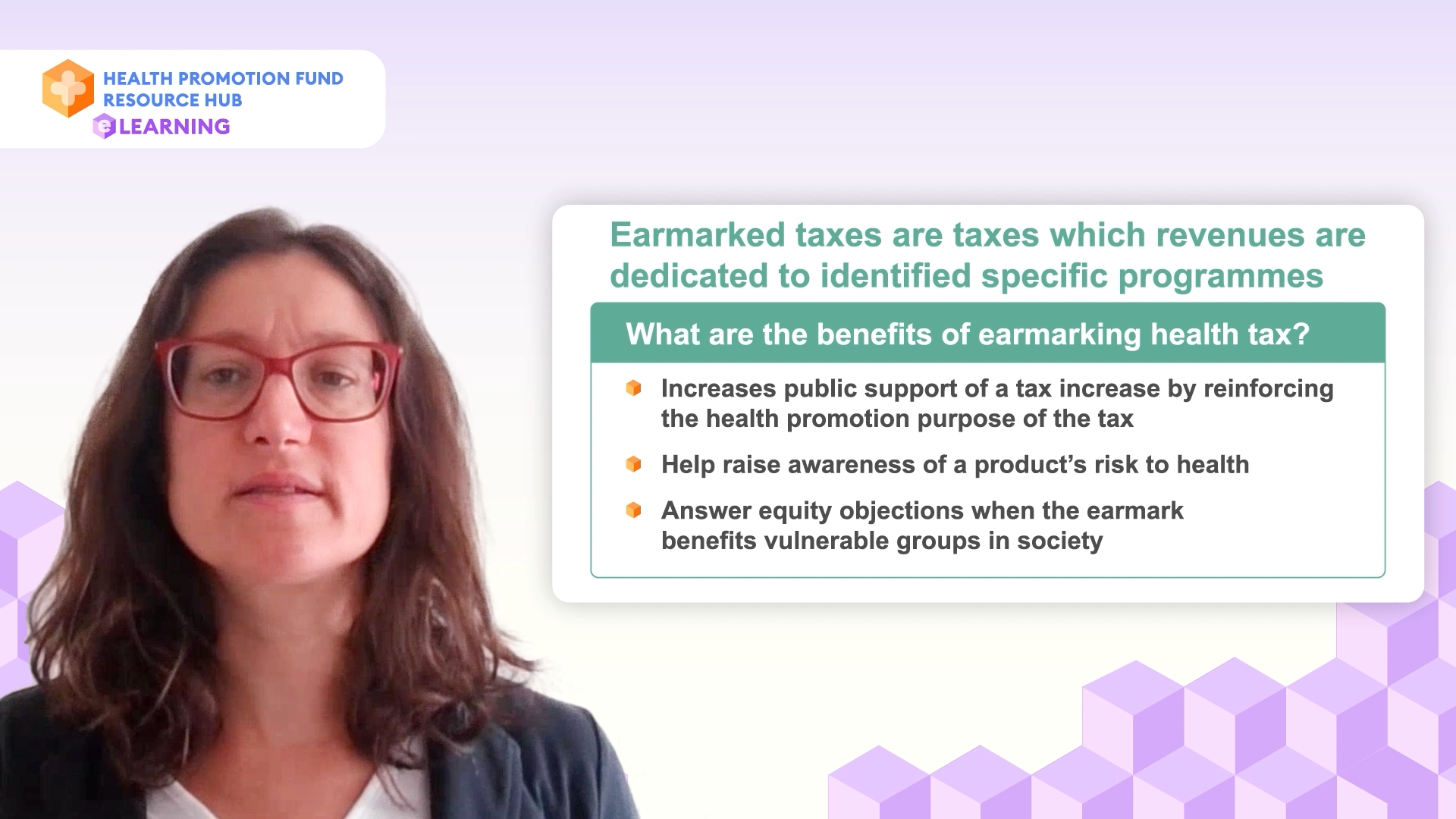

We have seen in the previous section of this module that funding health through public sources is the most viable. Taxes in general are a sustainable means to finance health. We will look now at the specific case of health taxes and at the concept of earmarking health tax revenues for health purposes. Earmarked taxes are taxes which revenues are dedicated to identified specific programmes. So what are the benefits of earmarking health taxes for health programmes? First, it increases public support of a tax increase because it reinforces the health promotion purpose of the tax. It also helps raise awareness of a product’s risk to health, and it specifically answers equity objections when the earmark benefits vulnerable groups in society.

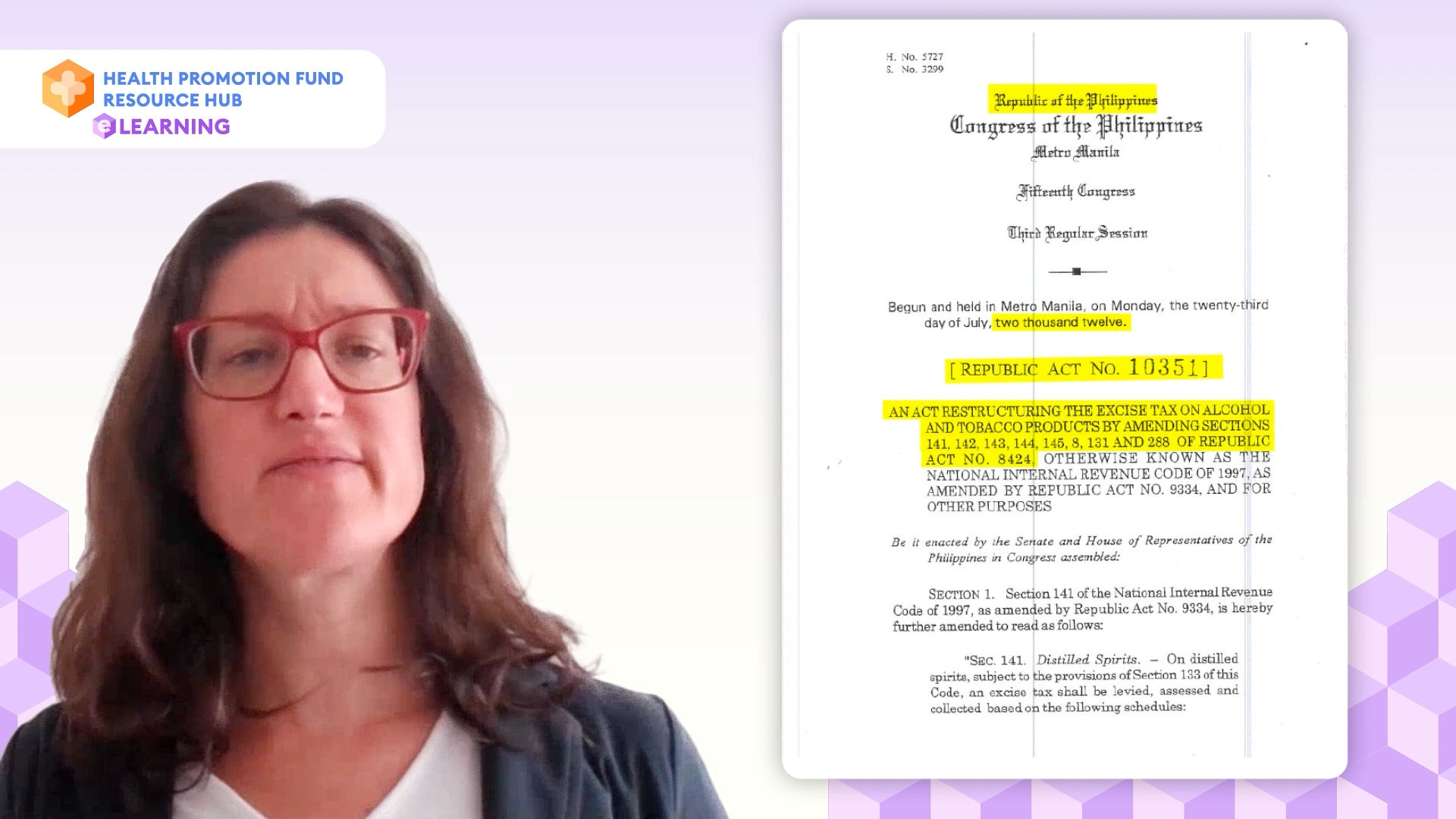

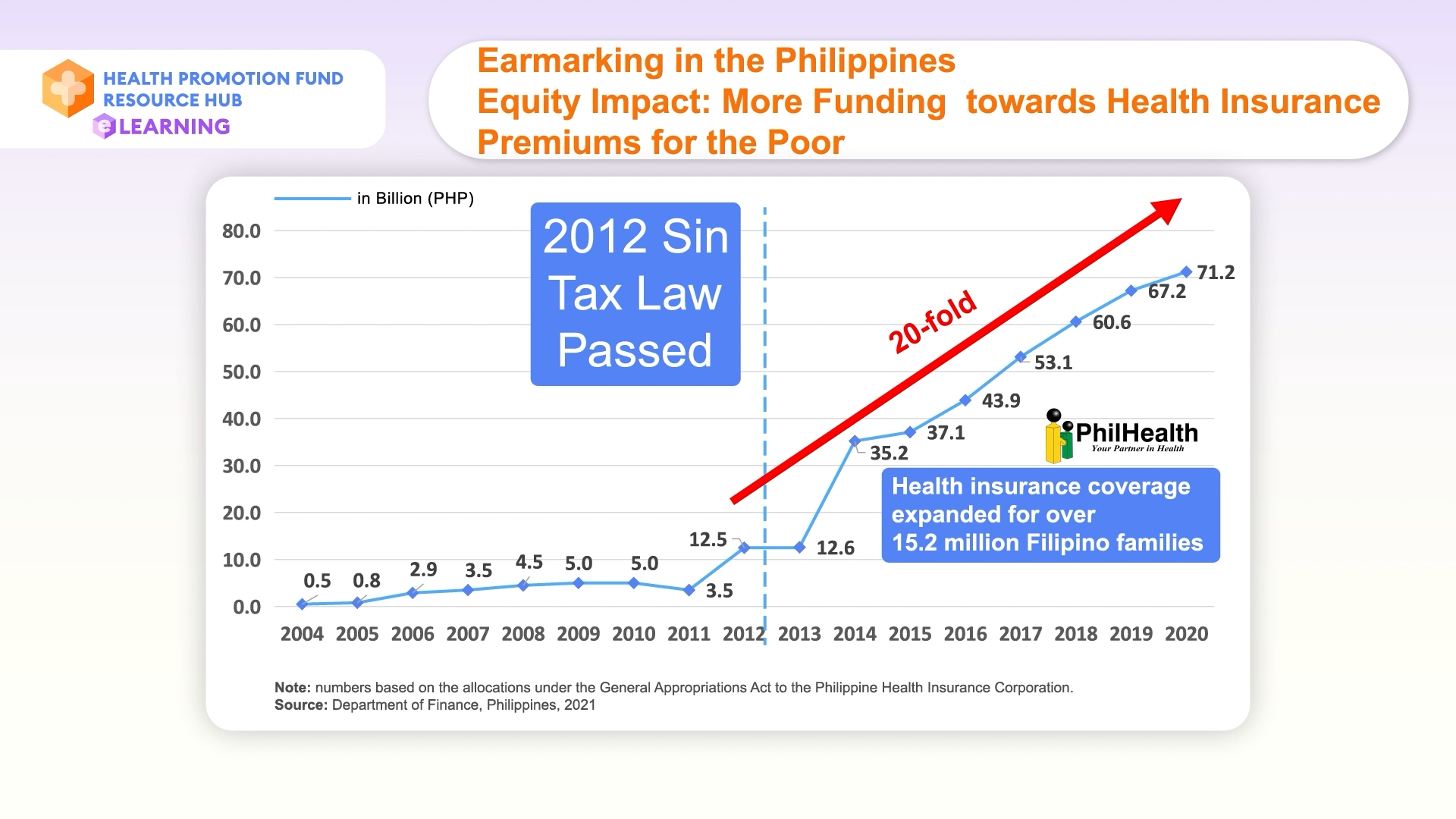

Let’s look now at the case of the Philippines and health taxes from a sustainable financing and equity lens. We know that the landmark sin tax law that was passed in 2012 made a large reform on tobacco and alcohol taxes and increased them significantly.

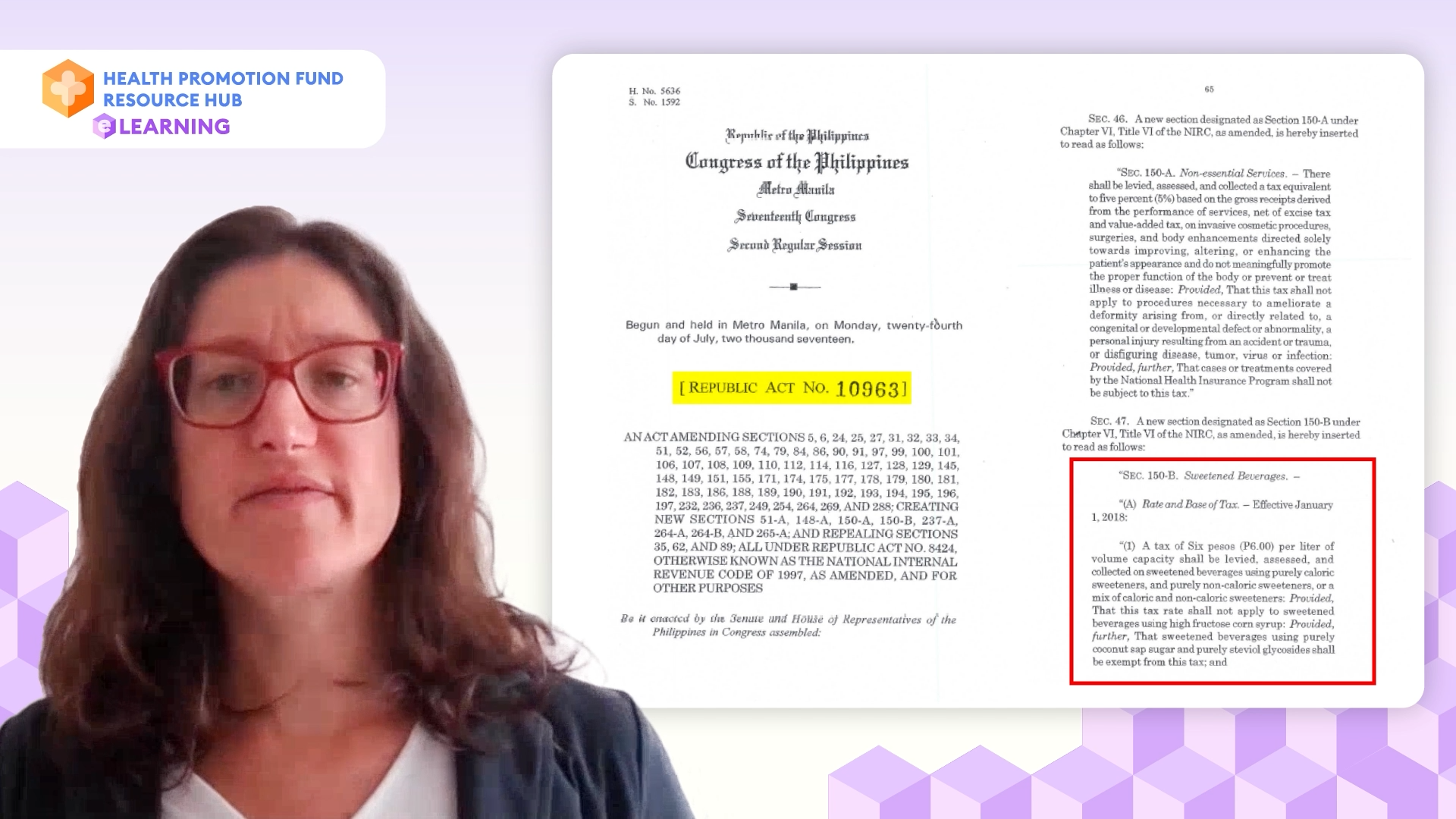

The tax on sugar-sweetened beverages (SSBs) was also introduced shortly after.

Additional revenues from those taxes were allocated mainly to fund the health insurance premiums for the poor therefore moving closer towards universal health coverage. The graph here shows the increase in the national health insurance premiums for the poor for PhilHealth, the National Health Insurance Programme, which allowed to expand health insurance coverage for over 15.2 million Filipino families.

We can see how between 2012 before the Sin Tax Law and now (2020) the budget increased 20-fold. This is really a very impressive positive development both for health and equity for the Philippines.

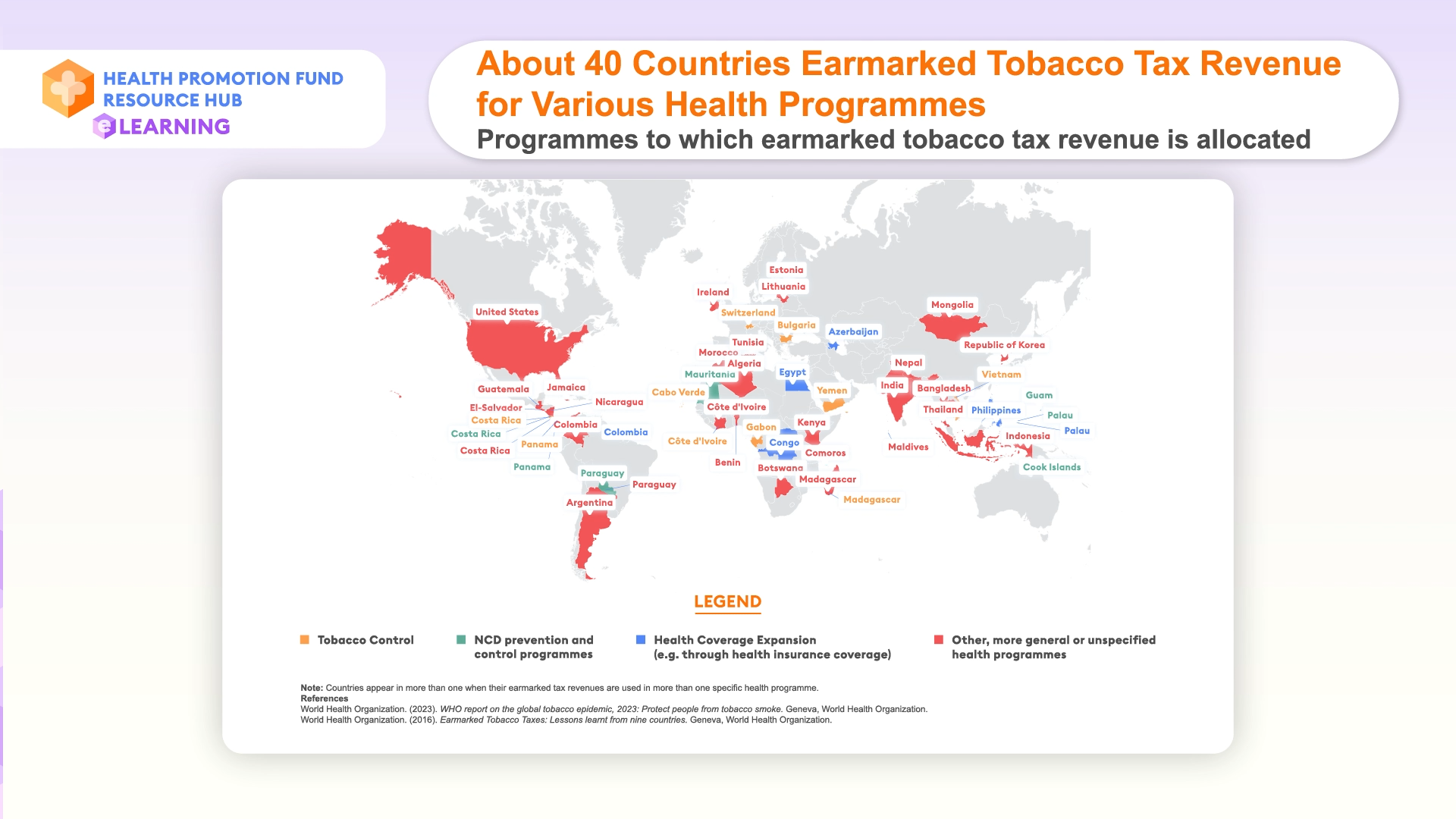

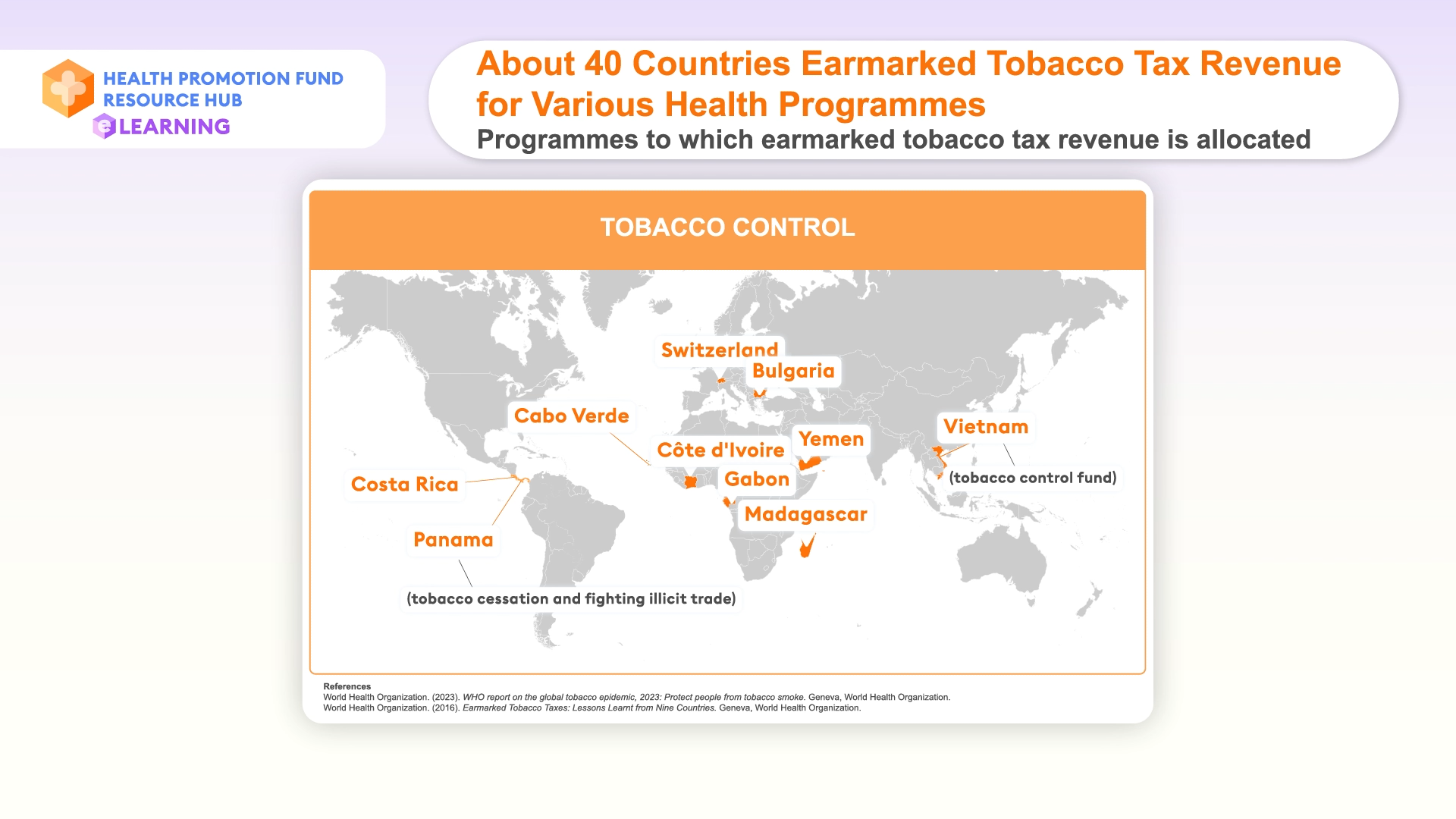

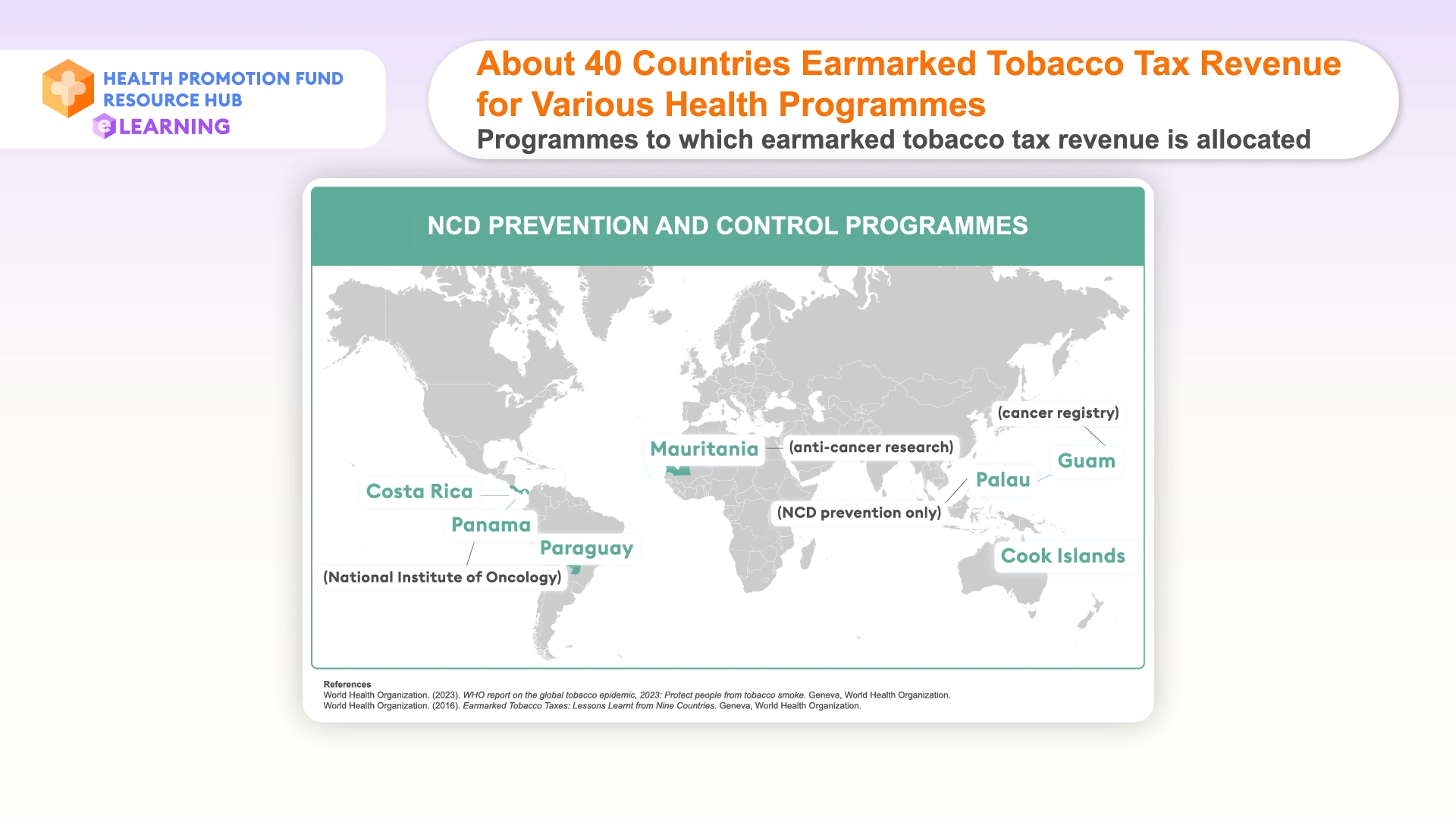

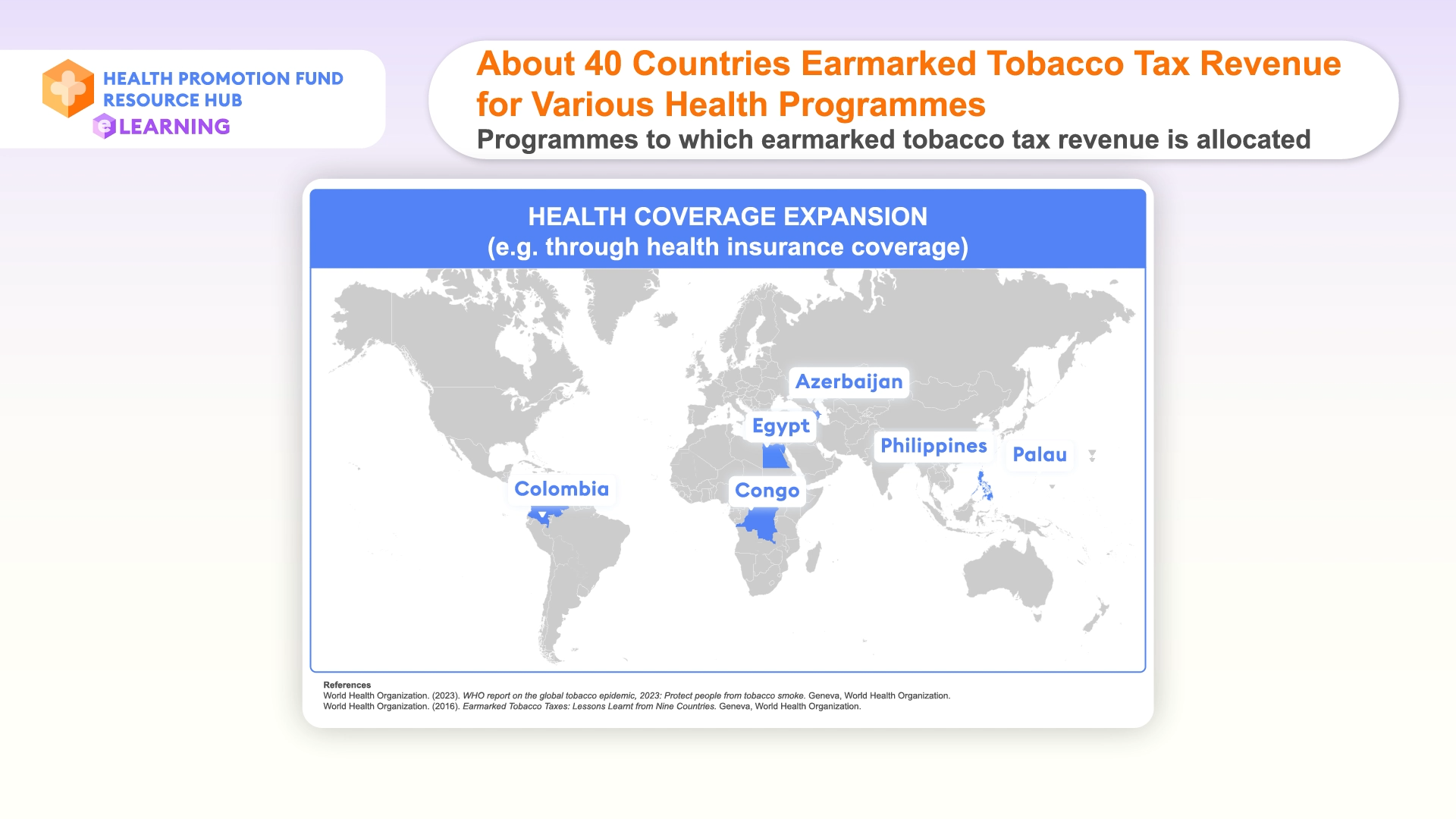

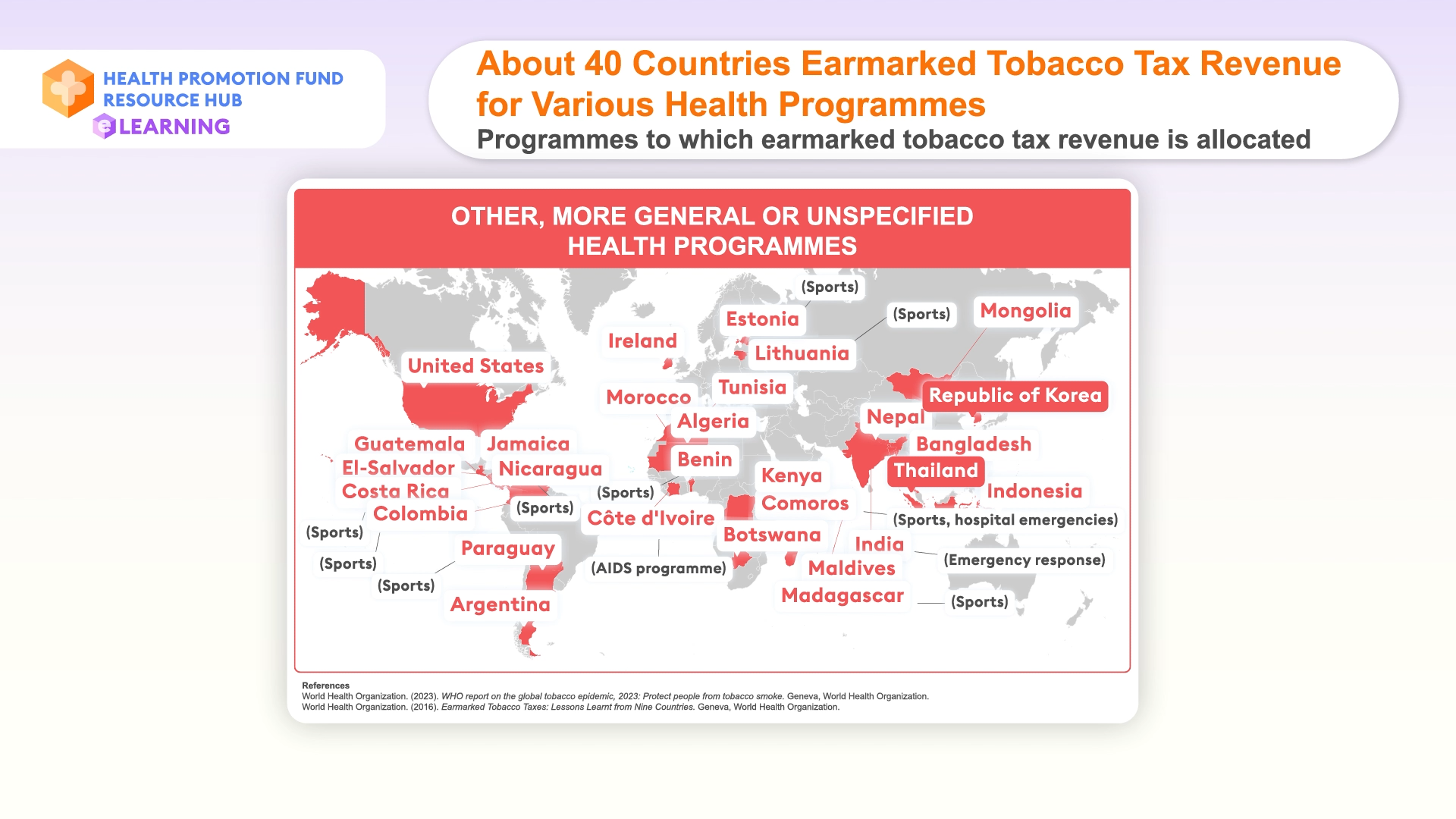

Looking at tobacco, this is the list of countries that are known to earmark their tax revenues for most it’s part of the revenues from tobacco to health programmes. In 2020, there were 39 countries around the world that earmarked their tobacco tax revenues to some type of health programmes with more countries adopting earmarked taxes for health over the years.

You can see some countries use the revenues specifically for tobacco control, others for broader Non-Communicable Disease (NCD) prevention and control programmes, others use them for health coverage expansion like we saw earlier in the Philippines and most use them for other or unspecified health programmes but also for health promotion such as Republic of Korea and Thailand.

Data on countries that earmark tax on alcohol or sugar-sweetened beverages for health programmes is less expanded and known but we can have an indication that at least in the case of sugar-sweetened beverages it is less common than for tobacco or alcohol. Data collected by WHO (World Health Organization) in 2022 show that around 19 countries out of the total of 140 countries where the data was collected earmarked alcohol taxes for health programmes, including for alcohol dependence treatment, Non-Communicable Disease (NCD) prevention and control programmes, health coverage expansion, health promotion or other programmes.

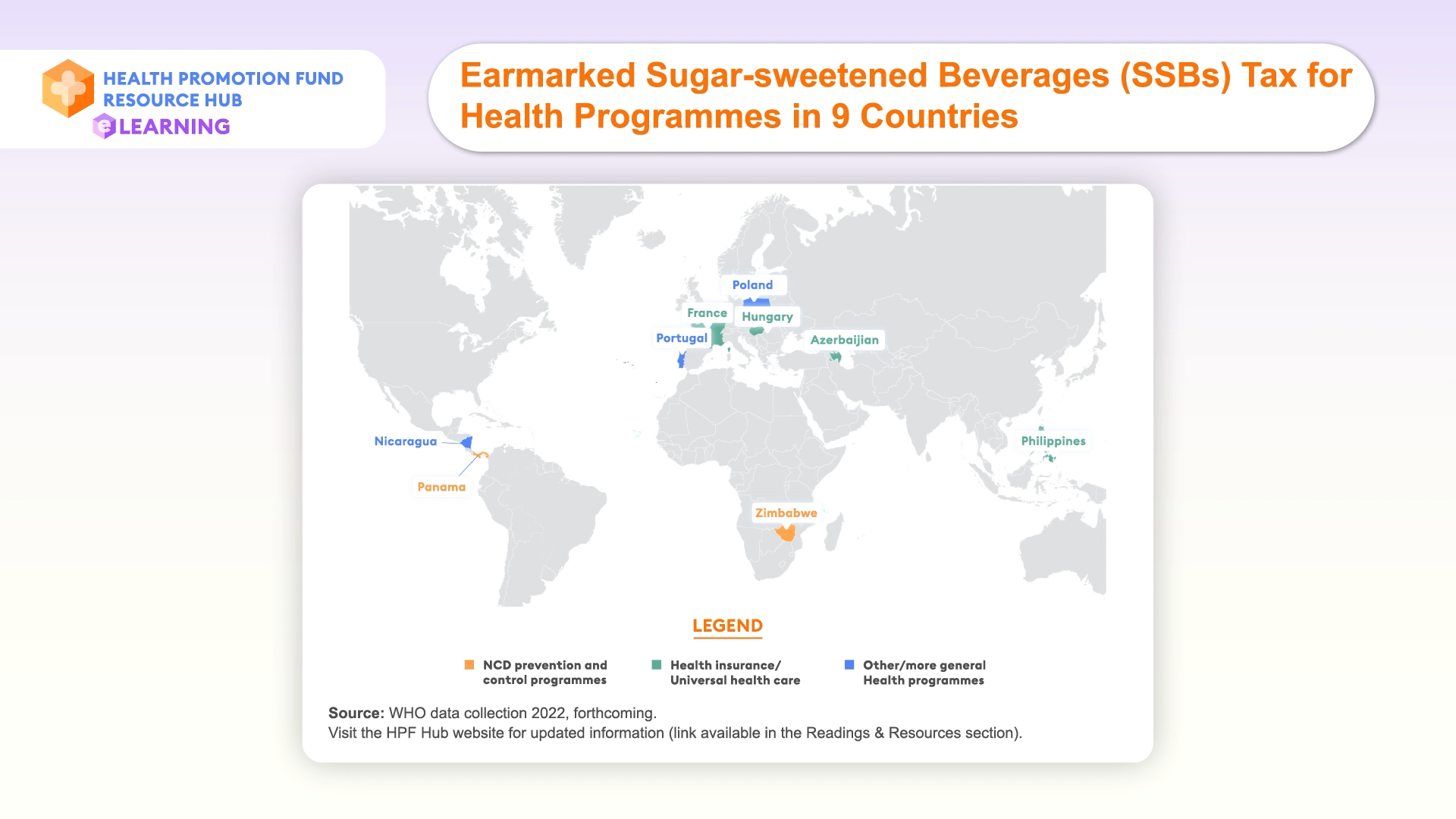

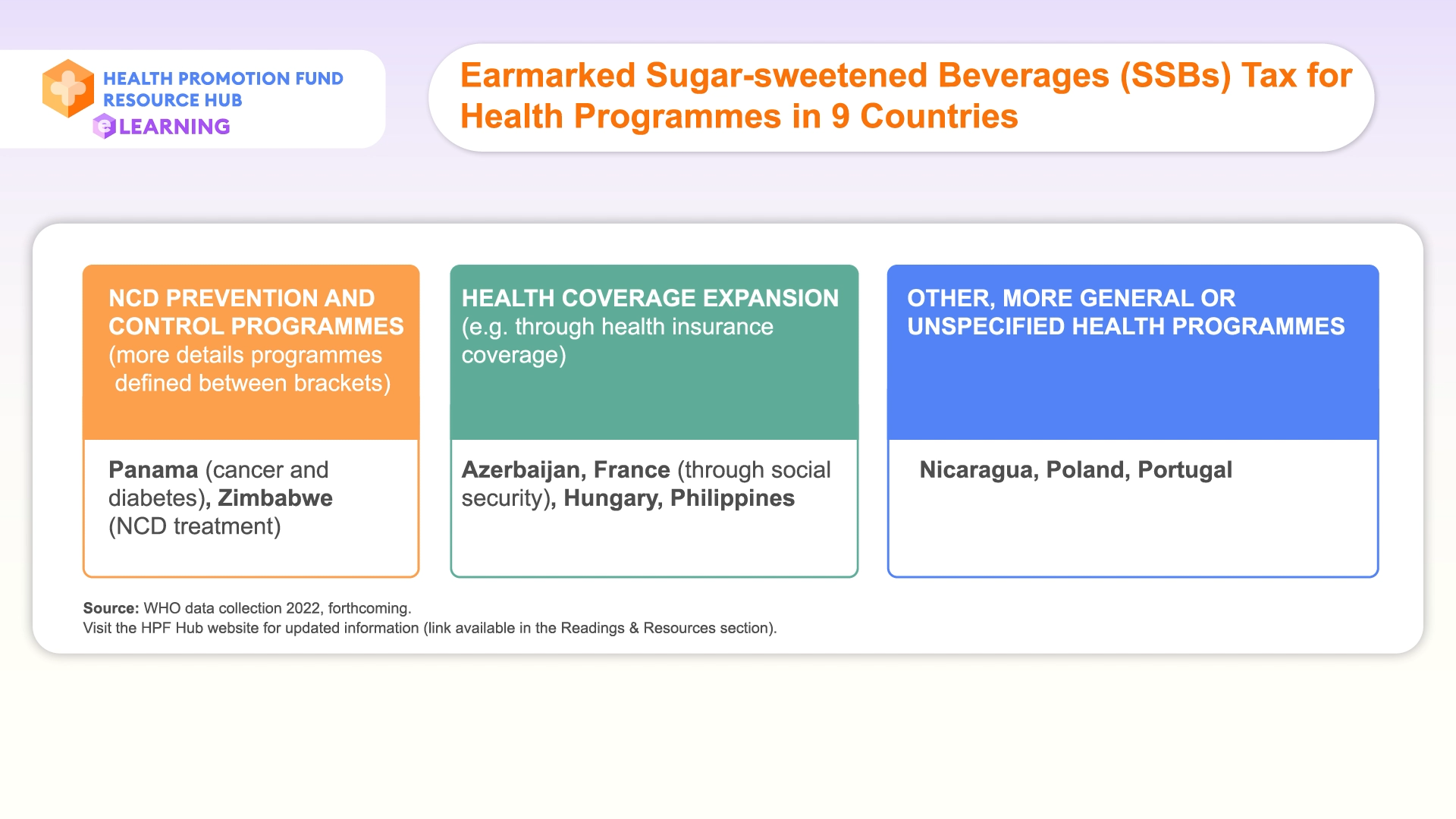

In the case of SSBs (sugar-sweetened beverages) tax, there are only 9 countries that are known to earmark the tax for health purposes.

Those also revolve around Non-Communicable Disease (NCD) prevention and control, health coverage expansion or more general unspecified programmes.

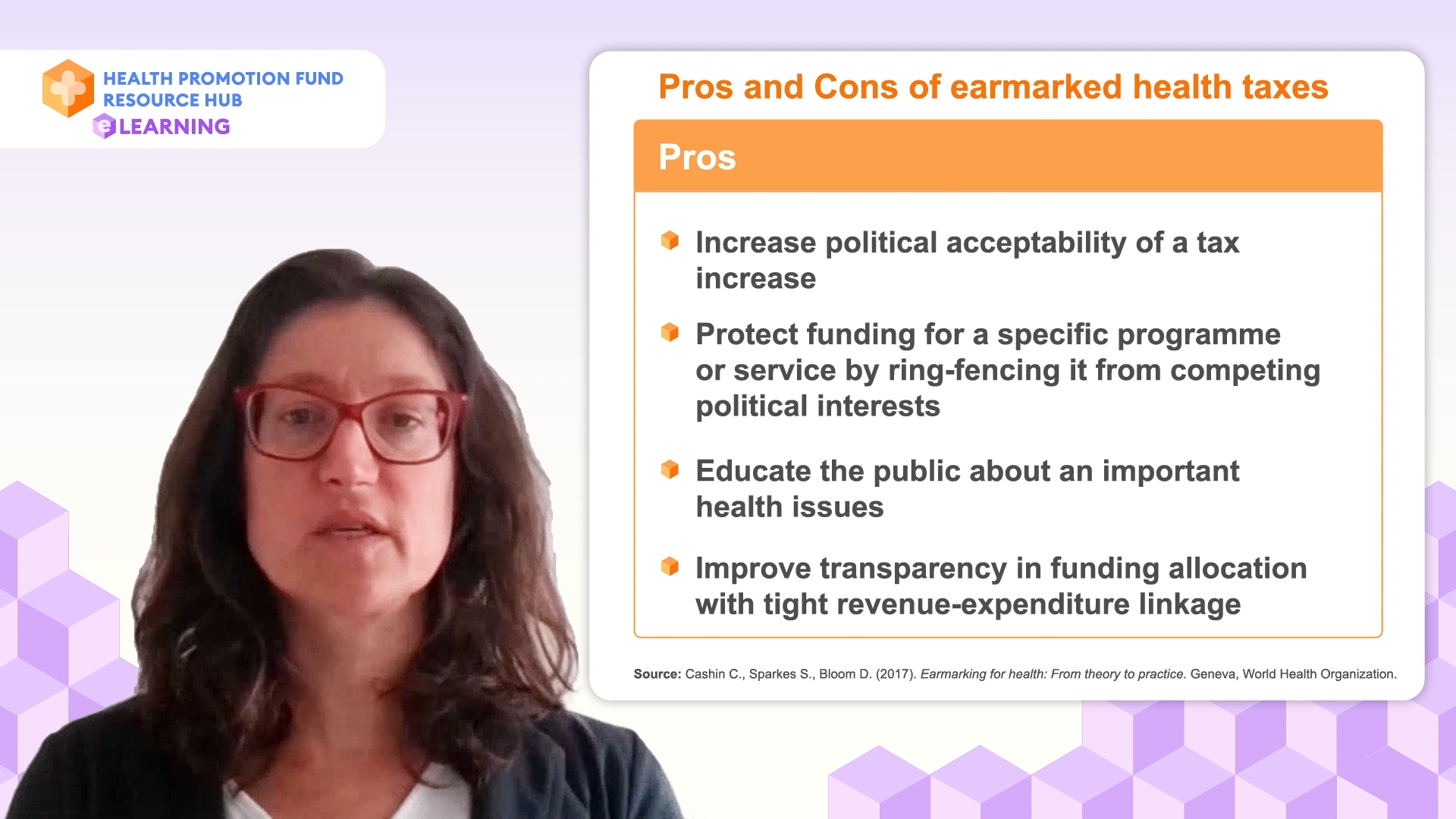

We have been talking about earmarked tax as one type of source of revenue for health but it is important to highlight that there are proponents and opponents of earmarked taxation and there is a list of pros and cons, at least in theory, for the earmark. The positives include Earmarking health taxes for health increase political acceptability of the tax increase. Earmarking can protect funding for a specific programme or service for example a low resourced programme by ring-fencing it from competing political interests. Because earmarking is usually publicized can also help educate the public about a health issue, such as for example NCDs, and how they can be prevented through policies like health taxes. Finally, earmarking improves transparency in funding allocation with tight revenue-expenditure linkage. This also increases accountability since people know where the money goes.

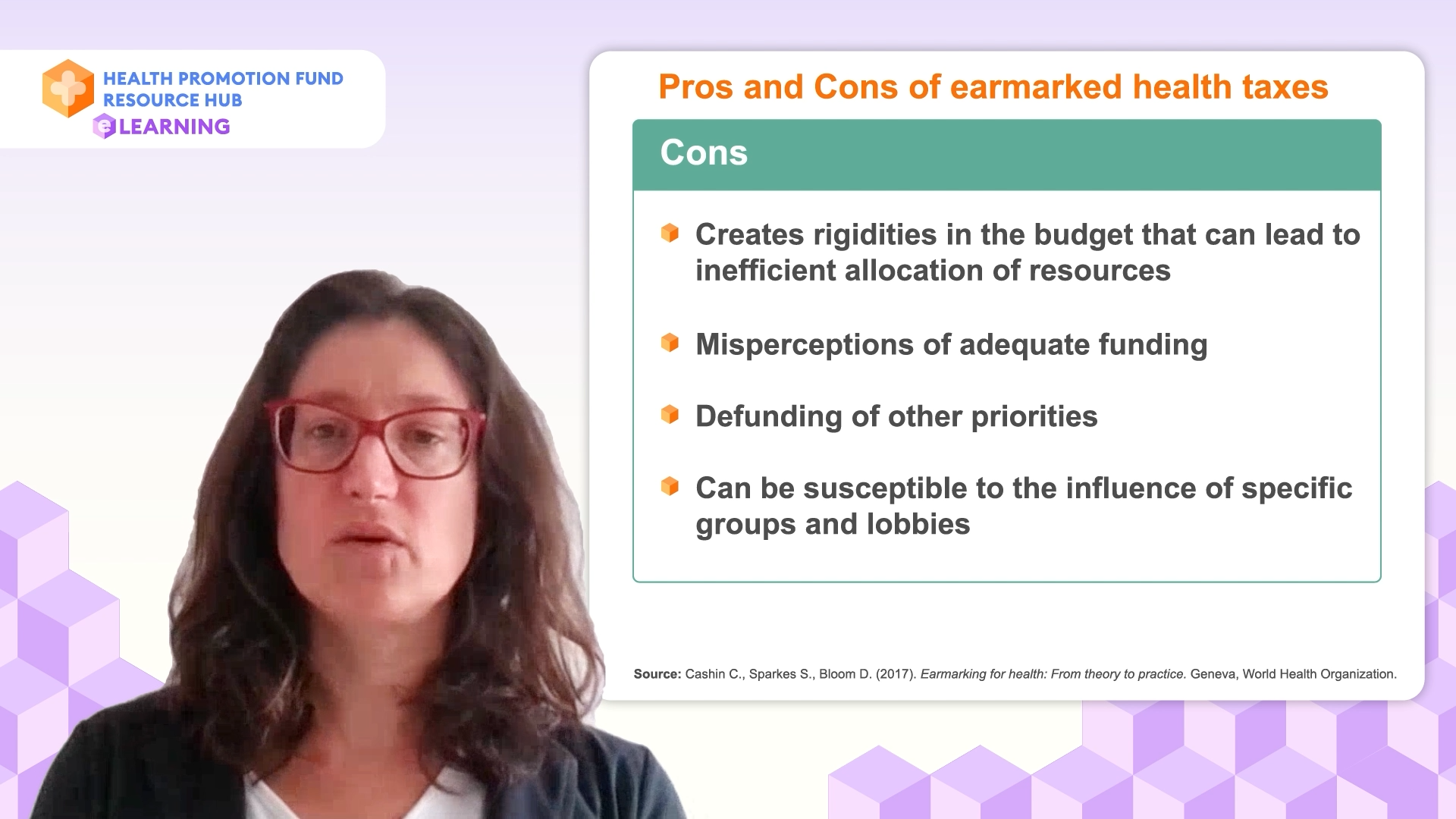

The negatives include Earmarking can create rigidities in the budget which can lead to inefficient allocation of resources. If for example too much money is allocated to a specific programme and not enough in another one that does not get this type of funding. In the same vain, if not well defined and resourced, earmarking can create misperceptions of adequate funding for the recipient programme and become a ceiling without opportunities to increase those funds if needed. Earmarking a specific programme can also run the risk of defunding other priorities. And finally, earmarked revenues can be susceptible to the influence of interest groups and professional lobbies that might work to obtain resources for their own benefit or for their own priorities without considering the broader effects.

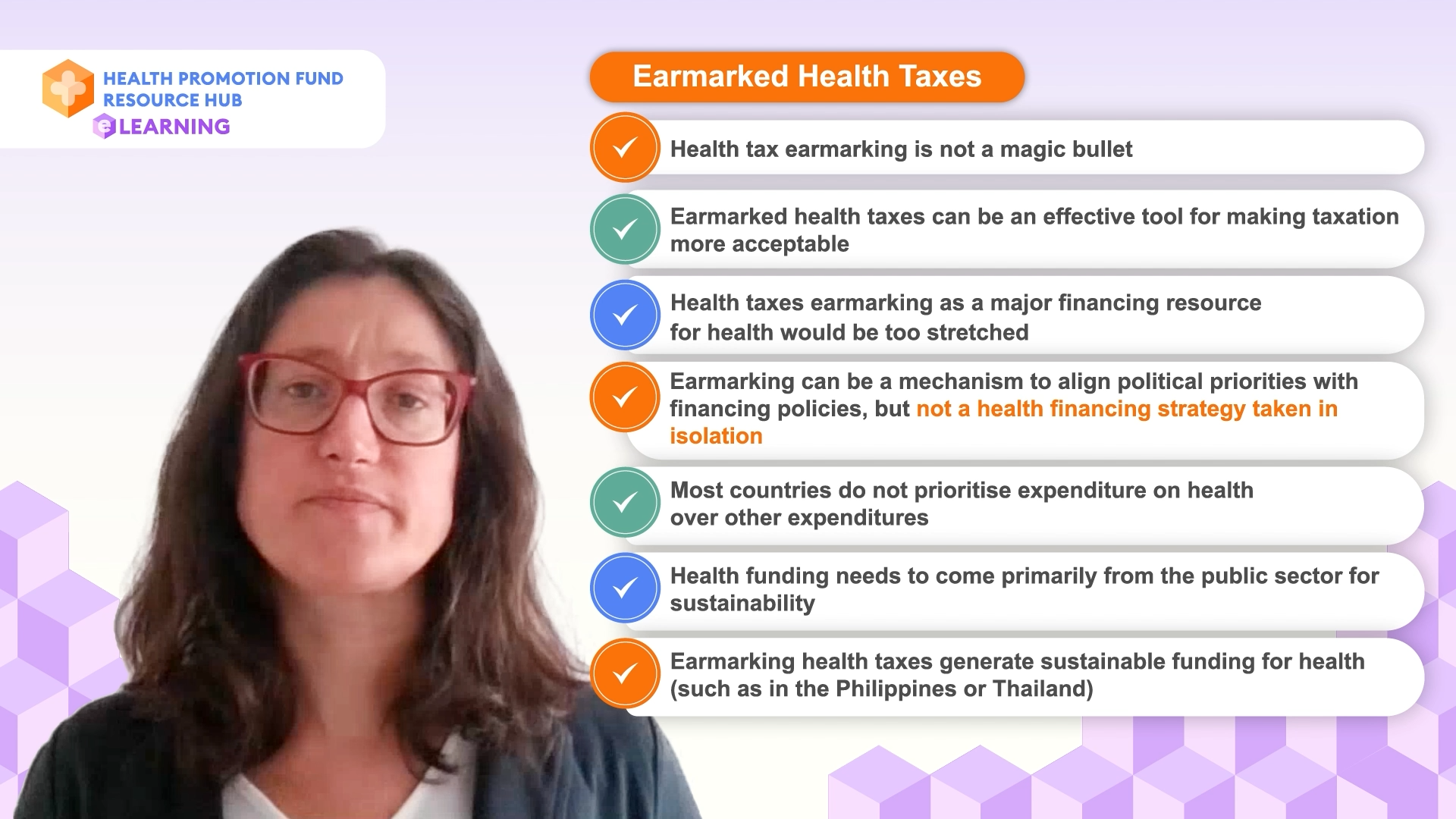

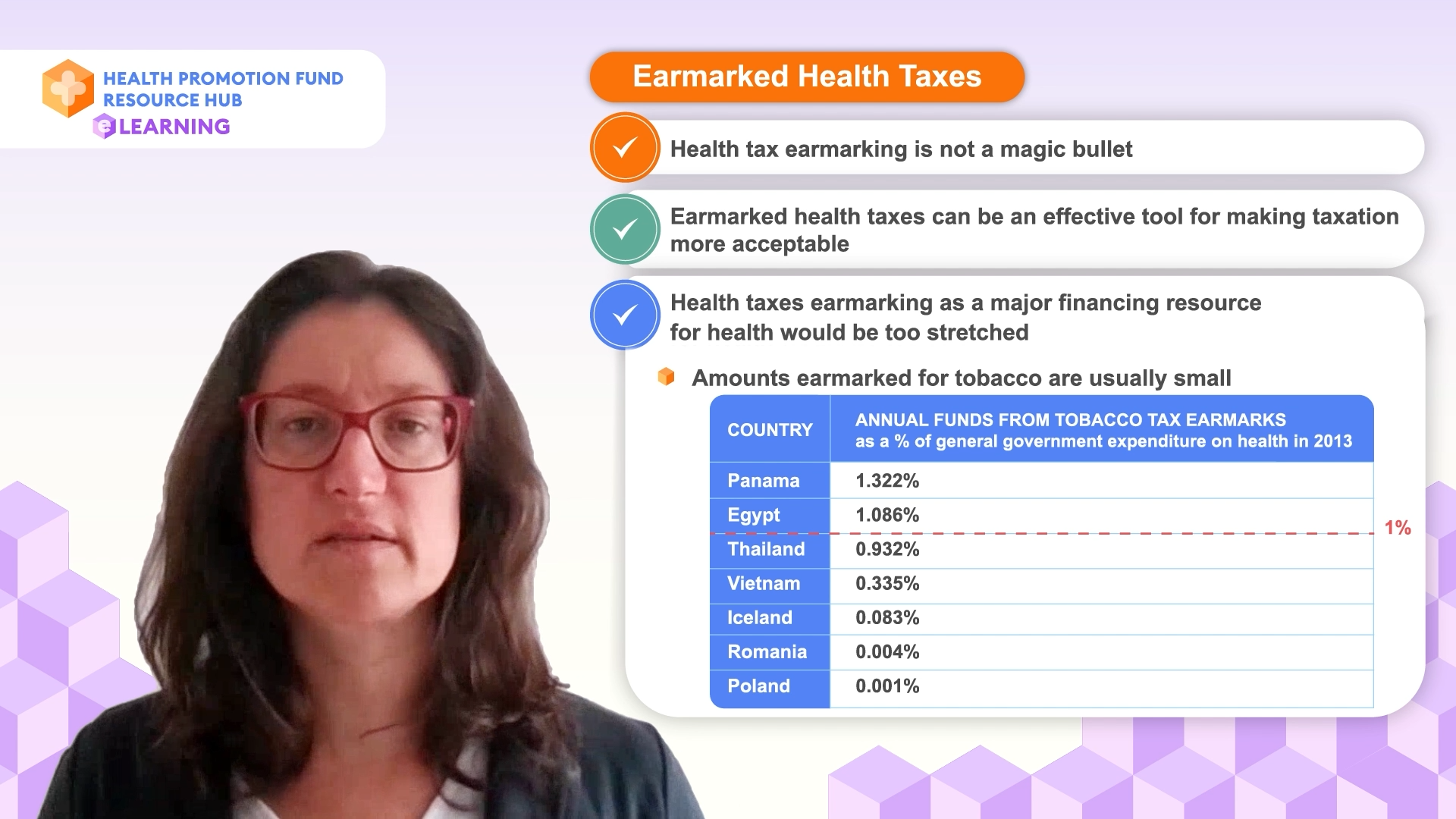

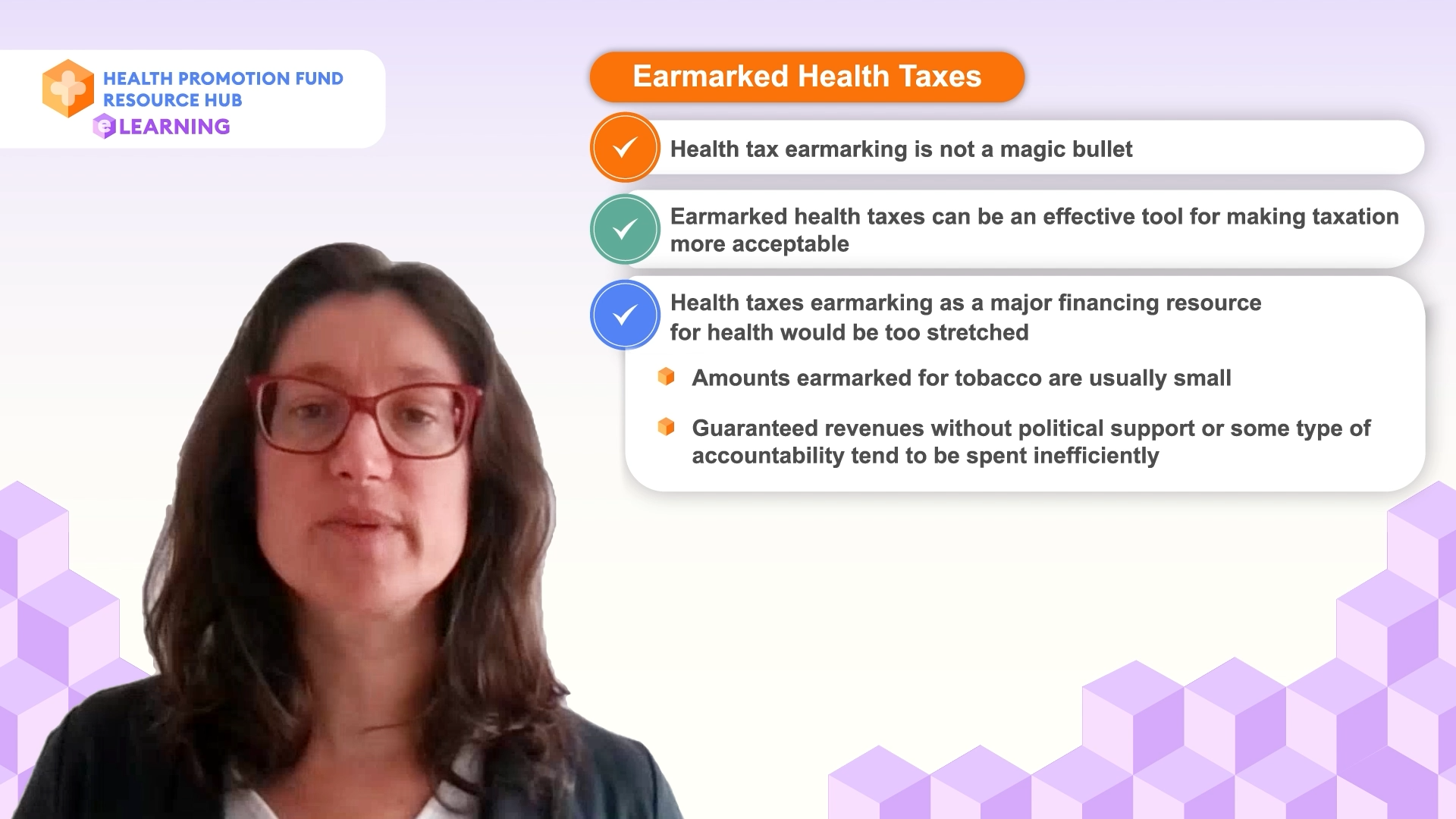

Despite all the benefits of an earmarked health tax for revenue purposes, it is important to put it back into perspective and note that it is not a magic bullet. While useful in some settings and can be an effective tool for making taxation more acceptable, health tax earmarking as a major financing resource for health would be too stretched. As you can see in the table here for tobacco the amounts earmarked are usually small, they are usually well below 1% of the general government revenues on health and are therefore not sufficient on their own to fund health.

Also, as experience from countries show, guaranteed revenues without political support or some type of accountability tend to be spent inefficiently and are short lived.

In sum, earmarking can be a mechanism to align political priorities with financing policies, but it cannot be a health financing strategy taken in isolation.

In conclusion, we have seen that countries all over the world still do not prioritize expenditure on health over other expenditures. We also know that for health funding to be sustainable, it needs to come primarily from the public sector, which is still not the case for most low-and-middle-income countries, especially low-income countries. Earmarking health taxes is one way to fund health in a sustainable manner and success stories like from the Philippines or Thailand are here to prove it.